Macroeconomic situation

The International Monetary Fund (“IMF”) estimates that in 2022 the global GDP increased by 3.4%, while the GDP of Poland increased by 4.9%. The data reveal that Q4 2022 was better that expected and the improved outlook on the global economy results above all from the slowing down inflation rate, among others due to the adjustment of prices on the raw material market, and from China’s abandoning the “Zero COVID” policy, which paralyzed the economic activity in that country.

As the main threats to the development rate of the global economy, the IMF lists, among others, the wave of COVID-19 cases in China, which will delay a recovery there despite the abolishment of the pandemic-related restrictions, the escalation of Russia’s war against Ukraine, the credit crisis related to the tightening of the monetary policy, and the fragmentation of value added chains (i.e. reversal of benefits stemming from globalization).

The IMF estimates that the GDP in the USA grew by 2% in 2022. The economic activity in the euro area, in turn, increased in 2022 by 3.5% according to IMF’s assumptions, and the European economies proved more resilient than expected, partly thanks to a mild winter. The Chinese economy grew by 3% in 2022, which was considerably below the official target of 5.5%, and the recurring blockages due to the COVID-19 pandemic and the downturn in the real estate market made the pursuit of economy activity difficult. In late 2022, in turn, China opened rapidly again, which led to a business recovery.

Global economic situation in 2022

The U.S. economy grew by 2.1% in 2022 after a 5.9% hike the year before. The biggest contributors to U.S. growth were consumer spending, growth of inventories, government spending, and foreign trade. China, the world’s second largest economy, still grew slightly faster. According to government statistics, China’s economy grew by 3% in 2022, compared to the ruling party’s target of 5.5%, making it the lowest growth rate in nearly half a century. This low performance was affected by the pandemic lockdown policy, which was only eased at the end of the year.

According to the European Commission’s medium-term forecast published in February 2023, GDP growth in 2022 is estimated at 3.5% for the EU and for the euro zone. The published data show that economic growth was recorded by almost all countries in the group, albeit to varying degrees. Ireland’s GDP experienced the strongest growth of 12.2%. According to the European Commission, Germany (+1.8%) and Latvia (+1.8%) saw the smallest increases. The weakness of the German recovery is primarily due to problems in the automotive sector, which continues to be hampered by government restrictions and consumer caution. Another contributing factor was a series of tensions in the supply chain for parts and components. The economies that grew the fastest in 2022 were Portugal (+6.7%), Malta (+6.6%), Croatia (+6.3%), Greece (+5.5%), Hungary (+4.9%) and Poland (+4.9%). Estonia was the only country to record a decrease (-0.3%).

Economic situation in Poland in 2022

According to a preliminary estimate by Statistics Poland, Poland’s economy slowed down noticeably in 2022, but GDP still grew by 4.9% for the year as a whole, following a 6.8% increase in 2021. As a result, the darkest scenarios from the beginning of last year that suggested that the Polish economy might enter a period of recession after the war and in the face of the energy crisis never materialized.

One of the driving forces of our economy was the state of industry, which was positively affected by the growing demand from abroad. In 2022, industrial production sold grew by 9.3%. Although this figure was worse than in 2021, it should be viewed positively, especially in the context of a recovery after the pandemic year of 2020.

According to Statistics Poland, economic growth in 2022 was driven by inventories, which accounted for 2.9 p.p. of the 4.9% GDP growth. Other positive factors included: private consumption (+1.7 p.p.) and investments (+0.8 p.p.). At the other end of the spectrum were the contributions of net exports (-0.4 p.p.) and government consumption (-0.1 p.p.).

According to the International Monetary Fund’s latest estimates, the economy of Poland will grow by 0.3% in 2023. In the following two years, growth is expected to accelerate to 2.4% and 3.7%, respectively.

As the Polish economy is highly dependent on and closely linked to economic conditions in the EU, which is dependent on global markets, these factors will continue to determine the direction and strength of developments in the domestic economy. For Jastrzębska Spółka Węglowa, the most important areas of the macroeconomic environment are those that may materially affect the future development of the Group, namely the markets for coking coal, coke and steel.

Forecast for 2023

The World Bank’s latest economic outlook data shows that the global economy will experience a strong slowdown in 2023 due to rising inflation, higher interest rates, lower investment, and the economic impact of Russia’s attack on Ukraine.

According to World Bank’s predictions, global economic growth will be at 1.7% in 2023 and 2.7% in 2024. The sharp decline in growth will affect most countries, and forecasts for 2023 have been revised downward for almost all developed countries and nearly 70% of emerging and developing countries. https://www.worldbank.org/pl/news/press-release/2023/01/10/global-economic-prospects

The International Monetary Fund has taken a similar view, predicting global economic growth to slow down to 2.9% in 2023 from 3.4% in 2022. The deceleration will have an impact on the world's three largest economies: the United States, the European Union and China, which will experience a significant slowdown.

Coal, coke and steel market

Steel market

The positive trend in steel consumption (observed in 2021) ended in Q2 2022 as a consequence of the drastic increase in gas and electricity prices. This influenced the steel market in the European Union, where many steel companies introduced production restrictions and temporary shutdowns of blast furnaces in H2 2022 in the conditions of an energy crisis, rising costs, and poor demand for steel products. In late November 2022, European producers shut down 10 blast furnaces (16.1 million tons of production capacities per annum). Two more blast furnaces were shut down in December 2022. The steel production reduction was caused by several factors: the economic slowdown in Europe, the high steel stocks, and the increase in gas and electricity prices. Furthermore, the CO₂ emission allowances as part of the ETS system, which do not apply to steel producers from outside the European Union, reached a record-breaking level in 2022, which made steel production in Europe uncompetitive.

According to the World Steel Association data, the global crude steel production was 1,878.5 million tons in 2022, down 4.2% compared to 2021. China, the largest steel producer in the world, produced 1,013.0 million tons of crude steel in 2022, down by 2.1% compared to 2021. At the same time, the crude steel production in China in 2022 accounted for 53.9% of the global steel production. India, the second largest steel producer in the world, increased the steel production by 5.5% to 124.7 million tons in 2022 relative to 2021, while the crude steel production in Japan dropped by 7.4% to 89.2 million tons in 2022. The crude steel production in the EU member states decreased by 10.5% to 136.7 million tons in 2022 relative to 2021, while Germany, the largest European steel producer, produced 36.8 million tons of crude steel in 2022, i.e. 8.4% less relative to 2021. Among 10 top steel producers in the world, only Iran and India recorded a steel production growth in 2022 relative to 2021.

In Poland, crude steel production in 2022 was approximately 7.7 million tons, i.e. 8.6% lower than in 2021. The considerable drop in production of steel and steel products was caused by the shutdown of one of the blast furnaces in the ArcelorMittal steelworks in Dąbrowa Górnicza in September 2022.

World Steel Association szacuje, że popyt na stal w światowej gospodarce spadł w 2022 roku w porównaniu z 2021 rokiem o 3,2% do 1,8 mld ton, zaś w krajach UE (razem z Wielką Brytanią) zmniejszył się w 2022 roku o 3,5% w stosunku do 2021 roku do poziomu 158,9 mln ton.

According to the European Automobile Manufacturers Association’s (“ACEA”) data, the quantity of new passenger cars registered in the EU decreased by 4.6% to 9.3 million in 2022 relative to 2021, mainly due to the shortage of components in H1 2022. Despite the improved market situation in H2 2022, the quantity of cars registered in entire 2022 was lower only in 1993, when 9.2 million new vehicles were registered. Among the four largest EU markets, the quantity of new passenger car registrations increased only in Germany in 2022, by 1.1% relative to 2021.

The average annual prices of flat (hot rolled coils – HRC) and long steel products (reinforcement bars) displayed differing trends in 2022. The average annual price of HRC on the European market (Northwestern Europe) dropped by 18.1%, while the average price of reinforcement bars surged by 18.0% relative to 2021. The price rebound in late 2022 resulted from the replenishment of stocks and the earlier steel production cuts.

Steel production and prices of steel products in the EU (USD/t)

Chart. Steel production [m tons]

Chart. Steel prices on the European market [USD/t]

Source: World Steel Association, Platts

Coking coal market

The coking coal market is a global market. Coking coal prices in overseas trade are driven chiefly in the relations between Australian suppliers and Asian clients. The Group sets coal prices based on published price indexes, taking into account differences in quality between the Group’s coal grades compared to index coal grades and the bonus it derives from its geographical location.

2022 was characterized by strong volatility in the target markets of the Group: steel, coking coal, coke as well as energy and energy fuels. Disturbances in coking coal supply that affect the global prices occurred from H2 2021. In 2022, the armed conflict in Ukraine and the sanctions imposed on Russia strongly affected the macroeconomic situation in Europe and the world, in particular the energy and energy commodity markets. In the situation of a limited coking coal supply maintaining for several quarters, the outbreak of the war in Ukraine has caused great uncertainty for steelmakers regarding security of supply of raw materials, providing the impetus for a short-term record-breaking increase in coking coal prices, exceeding historical highs by 200 USD/t. The prices of hard coals exceeded 670 USD/t in the peak period (as of 14 March 2022). In the following months, the prices steadily declined, reaching pre-war levels in June 2022.

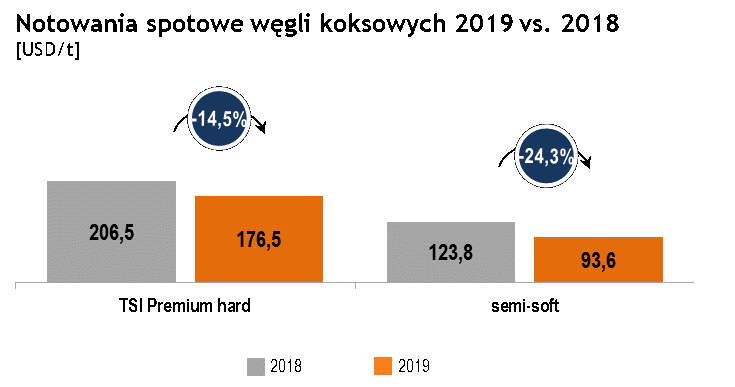

The average TSI Premium HCC index in Q1 2022 was 487.80 USD/t and fell 8.7% down to 445.52 USD/t in Q2 2022. In Q3 2022, the prices dropped again by 43.9% to 249.75 USD/t relative to Q2 2022, and in Q4 2022 the average TSI Premium HCC prices rose by 11.4% to 278.13 USD/t relative to Q3 2022. The average daily price for the TSI Premium HCC index in the full year of 2022 was USD 363.71, and was up 61.1% than in the previous year. Compared to hard premium coal grades, semi-soft coal grades reported greater price increases; the average annual price in 2022 was up 84.3% versus the previous year.

To mitigate the risk of fluctuations in daily index prices, JSW usually sets reference prices for negotiations with its customers based on HCC FOB Australia premium hard coking coal prices with the average being derived mostly using two methods:

- using the benchmark price determined according to the Nippon Steel method – quarterly reference price: average of the first two months in a given quarter and the last month of the preceding quarter for the S&P Global Platts Premium Low Vol FOB Australia index,

- the (Q-1) price designation method – quarterly reference prices calculated on the basis of average prices from the previous quarter for The Steel Index (TSI) – reference price for premium HCC coking coal used to set forward contracts.

The average price of coking coal JSW commanded in a given quarter is affected by the prices from five months (the previous quarter and the first two months of the current quarter), which averages out sudden fluctuations and contributes to greater stability of JSW's prices. The majority of the coking coal sales contracts comprise pricing formulas based on the aforementioned reference prices, which stabilizes the prices obtained by JSW in relation to Australian coal prices.

Considering the coking coal prices affecting JSW’s prices in a given year (the average price in October 2021 – November 2022), the growth in the average reference price for coking coal in 2022 versus 2021 was +95% (TSI Premium Hard: 191 USD/t in 2021; 372/t USD in 2022).

JSW’s coking coal prices in relation to TSI Premium HCC prices [USD/t]

* the average quotation of TSI Premium HCC for 5 months covers the previous quarter and the first two months of the current quarter

Source: Platts, JSW data.

Steam coal market

The consequence of Europe's deep energy commodity deficit, following the introduction of sanctions on Russia, has been an unprecedented increase in gas and electricity prices and concerns about their availability during the winter. The sanctions imposed on Russia regarding the ban on the import of energy commodities, the restriction of the supply of steam coal, and gas and oil from Russia to the EU have led to the need to rapidly import steam coal from overseas markets contributing to an increase in the prices on world markets. The average price of steam coal in ARA ports was 229.6 USD/t in Q1 2022; an increase by 47.8% to 339.2 USD/t occurred in Q2; in Q3 2022 prices were 364.2 USD/t up 7.4% from Q2 2022, and in Q4 2022 there was a 34.6% decrease in the prices from Q3 2022 to 238.2 USD/t. The annual average price for 2022 was 292.8 USD/t and was higher by 137.5% compared to 2021 (123.3 USD/t).

According to the Polskie Sieci Elektroenergetyczne, the domestic consumption of electricity from 1 January to 31 December 2022 dropped 0.53% y/y to 173.48 TWh. The electricity generation increased in that period by 0.91% y/y to 175.16 TWh. In 2022, 87.76 TWh of electricity was generated in commercial power plants from hard coal (down 5.67% y/y), 46.98 TWh from lignite (up 3.55% y/y) and 10.00 TWh from gas-fired power plants (down 25.17%), while 18.31 TWh was generated from wind power plants (up 28.60% y/y).

The change in the market situation has also affected domestic steam coal prices. The Polish Steam Coal Market Index prices in sales to commercial and industrial energy sector (PSCMI 1) in Q1 2022 stood at PLN 291.59 per ton and increased by 11.7% to PLN 325.58 per ton in Q2 2022. In Q3 2022, domestic mining companies undertook renegotiations with customers, as a result of which PSCMI1 prices increased by 64.8% to 536.42 PLN/t compared to the previous quarter. In Q4 2022, the prices stood at 543.89 PLN/t, up 1.4% compared to Q3 2022.

In 2022, the PSCMI1 index showing steam coal prices in sales to the domestic commercial and industrial energy sector was 408.66 PLN/t and versus 2021 it surged by 64.4% (248.57 PLN/t).

JSW’s steam coal prices in relation to PSCMI 1 prices [PLN/t]

Source: ARP, www.polskirynekwegla.pl, JSW data.

Coke market

Poland is one of the main suppliers of coke in the EU market. Since the coke market is globalized, coke from Poland competes with supplies of this commodity not only from Europe but also from all other parts of the world, including China, Russia and Colombia.

Prices of blast furnace coke increased following the outbreak of war in Ukraine, but the appreciation was less pronounced than for Australian coking coal. The prices of Chinese CSR 64/62 coke increased from below 500 USD/t in February 2022 to 680 USD/t in the second half of March 2022. On the European market, in March 2022, CSR 64/62 blast-furnace coke prices increased by nearly 100 USD/t (compared to February 2022) to 700 USD/t. As in the case of coal, there was a gradual decline in coke prices in individual months.

The average price of Chinese coke (64/62 CSR) FOB China in Q1 2022 was 563.8 USD/t, in Q2 2022 it increased by 5.2% to 593.2 USD/t relative to Q1 2022, in Q3 2022 there was a decrease in the prices by 28.5% to 424.0 USD/t compared to Q2 2022, and Q4 saw a further decrease by 6.0% to 398.4 USD/t compared to Q3 2022. The Chinese coke prices in 2022 reached 493.5 USD/t on average, which means an increase by 2.7% relative to 480.6 USD/t in 2021.

In the European market, blast-furnace coke (64/62 CSR) CFR was priced at 636.7 USD/t in Q1 2022, with a 4.2% price increase to 663.3 USD/t in Q2 2022. In Q3 2022, the average coke price on the European market was 460.0 USD/t, down 30.7% from Q2 2022, and in Q4 2022 it fell 10.9% to 410.0 USD/t compared to Q3 2022. The prices of blast-furnace coke in the European market stood on average in 2022 at USD 542.5 per ton on a CFR Northern Europe Port basis, representing an increase of 17.9% compared to USD 460.0 per ton on CFR Northern Europe Port basis in 2021.

The negative impact of the war in Ukraine was felt increasingly more strongly in the European market in H2 2022. The consequence of Europe's deep energy commodity deficit, following the introduction of sanctions on Russia, has been an unprecedented increase in electricity and gas prices and concerns about their availability during the winter. This influenced the steel market in the European Union. Faced with the threat of an energy crisis, rising costs, and uncertainty in demand for steel products, many steel companies have introduced production restrictions and temporary shutdowns of blast furnaces. Following a relatively stable steel production level in the EU in H1 2022, it plunged by 14.8% in H2 2022 relative to H1 2022.

Coke production at integrated coke plants has been curtailed to a lesser extent than would result from blast furnace shutdowns. Coke oven gas production has become a priority. This has led to a periodic oversupply of coke on the market and a drop in prices. The increase in imports of raw materials, mainly steam coal from overseas, has led to greater strain on domestic seaports and rail routes, making the logistics of delivery to customers, in particular overseas shipments, more difficult.

The Coke Market Report estimates that the global coke trade volume plummeted to 5.4-5.5 million tons in Q4 2022 from approx. 7.0 million tons recorded in both Q2 and Q3 2022. The coke trade volume in Q4 2022 means the lowest quarterly result recorded since 2020. A clear drop in imported coke demand was visible in all world regions but the coke trade in Europe was exceptionally low.

Chart. Coke prices **

Source: Platts, C&AMR.

** taking into account the quotations affecting JSW’s prices in a given year (the average price from Q4 last year - Q3 this year), the increase in the average reference price of coke in 2022 versus 2021 was +65%

(blast-furnace coke on the European Market: 262 USD/t in 2021, 598 USD/t in 2022)

The prices of the coke sold by the Group are set at the turn of each quarter; to reflect the market terms of negotiations it is optimal to compare the prices commanded in a given quarter with the average prices in the previous quarter. Considering the prices affecting JSW’s prices in a given year (the average price in Q4 of last year – Q3 of the current year), the growth in the average reference price for coke in 2022 versus 2021 was 65% (blast-furnace coke on the European market: USD 362 in 2021; USD 598 in 2022).

Chart. JSW’s coke prices in relation to prices of blast furnace coke on the European market [USD/t]

* coke prices are set at the turn of each quarter in order to reflect the market terms of the negotiations. The optimal approach is to compare the prices obtained in the respective quarter with the average quotations from the previous quarter

Source: Platts, Coke & Anthracite Market Report, JSW data