Market and competitive environment

JSW Group is the European Union's largest producer of high-quality coking coal and a major producer of coke. The type and range of the Group's activities and products are largely sensitive to changes on the intertwined coal, coke and steel markets.

Coal market:

- global:

The coking coal market is global as demand for coking coal and coke largely depends on the condition of the steel industry, which uses the commodity in blast furnaces to produce pig iron - over 70% of steel is produced in blast-furnace technology. Coking coal is usually processed into coke at large steel-makers’ own coking plants and non-integrated (commercial) coking plants.

Global coking coal production (1 139.5 million tonnes/year) is highly concentrated in several countries. The largest producers of coking coal are China and Australia, which together have a market share of more than 75%. The largest exporters of coking coal include:

Table. Coking coal producers in 2019

| BHP Group -Australia | Teck Resources - Canada | Anglo American - an international group based in Great Britain | JSW Group - Poland |

|

|---|---|---|---|---|

| production | 42,4 mt | 25,7 mt | 22,9 mt | 10,2 mt |

| revenue | PLN 44,3 billion | PLN 11,9 billion | PLN 29,9 billion | PLN 8,7 billion |

| employment | ~ 72 000 | ~ 10 100 | ~ 63 000 | ~ 30 600 |

Chart. Largest producers of coking coal in 2019

China, the world’s largest producer of coking coal, is also a major importer of this raw material. All of its production ends up on the domestic market. Australia - the second largest producer of coking coal, behind China - exports nearly 100% of its production.

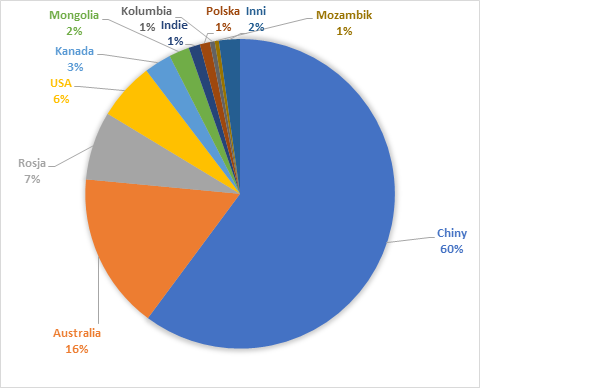

Global demand for coking coal depends on a single customer - China, whereas global supply depends on the main supplier - Australia, which together with other major exporters - USA, Canada and Russia - account for over 90% of coal supplies to the global market. The total volume of trade in coking coal is approx. 340 million tonnes (according to CRU data for 2019).

The level of global coking coal imports - aside from the supply-demand relationship between China and Australia - is also driven by one-off events such as adverse weather conditions, logistics or geological problems. These events are temporary and lead to alternative sources of import being activated.

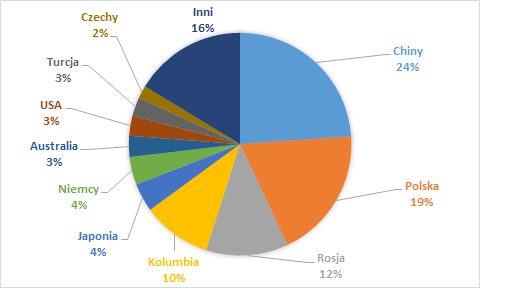

Chart. Largest importers of coking coal in 2019

- european:

Guaranteed stable deliveries of key raw materials at competitive prices are important to the European steel industry. A lack of sufficient own sources of supply means that the European Union is almost entirely dependent on the import of both iron ore and coking coal. In 2017, the European Commission emphasised coking coal’s critical raw material status by placing it on its list of 27 raw materials that carry the risk of supply shortages and the effects of which for the economy would be greater than in the case of other raw materials. The list is updated every three years.

Currently in the EU coking coal is generally produced only in Poland and the Czech Republic, which means that the European Union has historically had and continues to have a structural deficit of coking coal. Demand from the steel industry exceeds the production capacities in EU countries by approx. 40 million tonnes. The deficit of coking coal on the EU market is mainly made up by imports from Australia, USA, Canada, Russia and in recent years Mozambique and Colombia.

In the European Union, aside from JSW (with an annual output of approx. 11 million tonnes), coking coal is also mined by the Czech-based OKD (3.2 million tonnes of coal mined in 2019), which is systematically shutting down its mines. That company will conduct mining activities until 2030 at the latest.

In 2019, Great Britain announced that it will begin mining coking coal at West Cumbria Mining (WCM), a mine that is currently being built and is expected to be put into service in 2024. The British mine is expected to eventually produce approx. 3.5 million tonnes per year. Initially, WCM will produce about 0.5 million tonnes, with 80% sold on the European market.

As leading producer of coking coal in the European Union, JSW, while benefiting from a geographic advantage, is subject to general trends on the global market. With no quarterly benchmarks for coking coal, the determinant of global coking coal prices, having been published since Q2 2017, price negotiations are currently based on daily quotations for Australian or American coal.

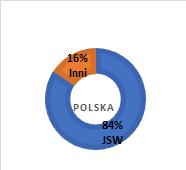

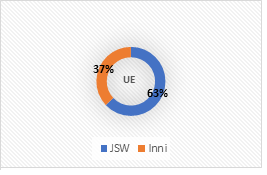

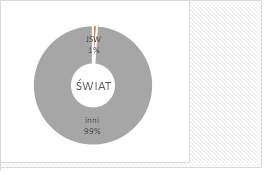

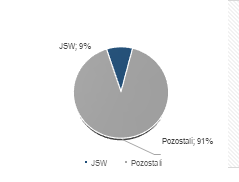

Chart. JSW's share in coking coal production in Poland, EU and globally

- domestic:

JSW is the only domestic producer of hard coking coal and a major producer of semi-soft coking coal. The other domestic producers mainly produce coal for energy purposes, with coking coal having a small share of their total production volume.

Coal companies in Poland usually produce coal for electricity and heating generation purposes. The largest domestic coal companies, aside from JSW, are: Polska Grupa Górnicza and Lubelski Węgiel "Bogdanka."

JSW Group is a major supplier of high-quality coking coal on the domestic and European market. The remaining portion of the coal produced by JSW is coal for energy purposes. Coal for energy purposes is used by JSW mainly to generate electricity and heating for own purposes. The remaining part of coal for energy purposes is sold to domestic energy enterprises. JSW Group, not a major domestic producer of coal for energy generation, is seen by customers in the domestic energy generation segment as a supplementary supplier, in connection with which JSW cannot independently shape market realities, rather having to adapt to the existing ones.

Chart. JSW's share in production of coal for energy generation purposes in Poland

The price of coal for energy generation purposes in Poland is largely driven by the situation on the domestic market and competition between domestic producers. The market for coal for energy generation purposes in Poland is largely dependent on the domestic economic situation, weather conditions, energy policy (prices of electricity, use of biomass, lignite-based electricity generation, share of subsidised renewable energy). Prices for coal for energy generation purposes to a limited extent follow the global trends in price indexes for spot transactions. While indexes set trends, the situation on the domestic market and competition between domestic producers are of key significance. Market prices for coal for energy generation purposes are determined by PSCMI (Polish Steam Coal Market Index). This is a group of price indicators for benchmark coal for energy generation purposes produced by domestic producers and sold on the domestic energy market (PSCMI 1 index) or the domestic heating market (PSCMI 2 index). These indicators are based on monthly ex-post data and express the sales price for hard coal (ex-works), with quality parameters optimised for customer needs.

Poland is the second-largest exporter of coke in the world, behind China.

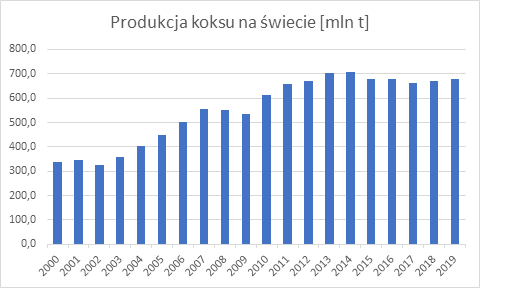

Just as in the case of coking coal, the coke market is global. Coke production is increasing and demand for coke mainly depends on the level of steel production in blast-furnace processes and changes in the technological processes for steel production. Coke production is mainly concentrated in Asian countries, which account for over 80% of global coke output. European Union members account for merely 6% of coke consumption, consuming approx. 41-43 million tonnes per year.

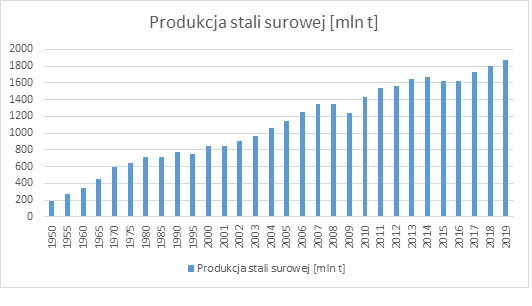

Chart. Global coke output [million tonnes]

Chart. Largest producers of coke in 2019

The European Union predominantly features coking plants integrated with steel works, which meet their needs using internally produced coke in the first place. At JSW Group, coking plants are independent, meaning that the entire coke output is for sale. Several independent coking plants are also located in Hungary, Czech Republic and Bosnia. JSW Group's advantage over other coke producers lies in the availability of raw material - a majority of integrated coking plants are mainly based on coking coal from own mines. Despite the fact that most of the European steelworks have their own integrated coking plants, they still require imports to a certain degree. On average, European steelworks meet 95% of their demand through their integrated coking plants. When reducing steel production, external supplies are cut first, which is why independent suppliers suffered the most in 2019.

The coke consumption structure globally and in the EU is similar: approx. 80% of coke is used for producing pig iron in blast-furnace processes and the other 20% outside of blast furnaces. A vast majority of coke is produced in coking plants owned by steel-makers. This production is for the internal purposes of steelworks owned by these steel-makers. Only a small volume (slightly over 4% of total production volume) is internationally traded.

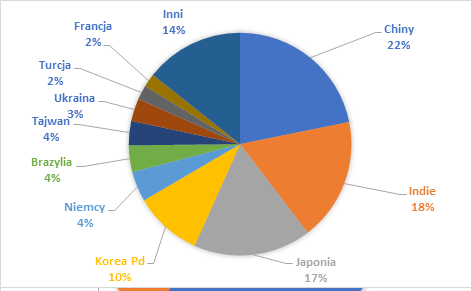

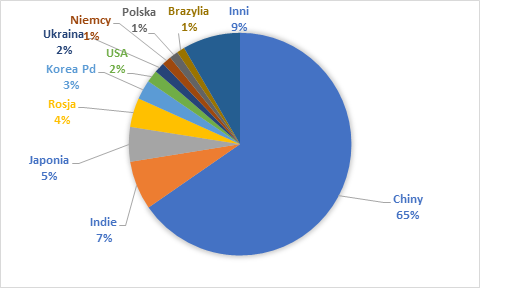

The total global trade of coke is estimated at approx. 30 million tonnes, with the EU accounting for approx. 11 million tonnes. The largest exporters of coke in 2019 were China (6.5 million tonnes) and Poland (5.4 million tonnes). These two countries account for over 40% of the coke trade volume.

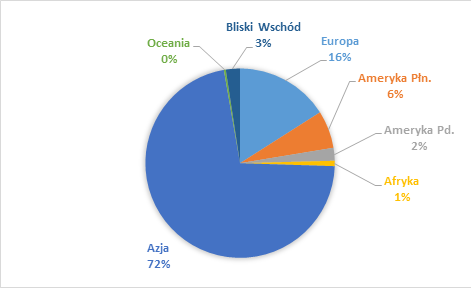

Chart. Largest exporters of coke. Share of the global market in 2019

The iron and steel industry is the largest and key customer for coke, where it is mainly used to produce pig iron in a blast-furnace process while finer types are used to produce agglomerates from iron ore that are then used in the production of ferro-alloys. Foundries that use high-quality foundry coke are also in this customer group.

The other types of coke are used for smelting non-ferrous metals (zinc, lead and copper), in the lime industry, chemicals industry (mainly to produce carbide), soda industry (production of glass), food sector (sugar refineries, dryers) and communal services sector (heating coke).

Approx. 780kg of coking coal is needed to produce 1 tonne of steel

The steel market is dominated by global steel-makers and steel production is largely concentrated in Asian countries. China remains the largest producer of steel.

Demand for steel is primarily generated by investments: in construction (approx. 34% of global steel consumption), road-building, energy and railways, as well as in the engineering and machinery industry (approx. 15% of global consumption), ship-building, household supplies (approx. 2% of global consumption) and automotive (20% of global steel consumption).

Steel production is still dominated by oxygen-blown converter technology using coke. It accounts for over 70% of the global steel production structure. Steel production in electric arc furnaces accounts for approx. 25% of raw steel output, while production in open hearth furnaces has a small and declining share.

Chart. Raw steel output [million tonnes]

The oxygen-blown converter process also dominates in the European Union but steel production in electric arc furnaces has a larger share than the global average.

Demand for steel and level of production and the prices obtained by producers set the market conditions for coking coal producers. They specify demand for coking coal and realisable prices for this raw material.

Chart. Produkcja stali w podziale na regiony świata

Tabela. Steel production by geographic region

| [million tonnes] | |

|---|---|

| China | 996,3 |

| India | 111,2 |

| Japan | 99,3 |

| USA | 87,9 |

| Russia | 71,9 |

Tabela. Najwięksi producenci stali

| [year] | |

|---|---|

| ArcelorMittal | ~ 96 million tonnes |

| China Baowu Group | ~ 67 million tonnes |

| Nippon SteelCorporation | ~ 49 million tonnes |

| HBIS Group | ~ 46,8 million tonnes |

| POSCO | ~ 42 million tonnes |