Macroeconomic environment

Global economic situation in 2021

The US economy grew by 5.7% in 2021 as the global economic "unfreezing" continued, after contracting by 3.4% in real terms in 2020. The biggest contributors to growth in the US were inventory changes and private consumption. However, the world's second largest economy, China, grew more dynamically. According to government statistics, China's economy grew by 8.1% in 2021 against a target of more than 6% set by the ruling party, the fastest growth rate in a decade.

According to data published by the European Commission, GDP growth in the European Union reached 5.3% in 2021 (and 5.3% for the eurozone). Nearly all countries in this group went through the recovery, although on varying scales. Ireland recorded the strongest GDP growth dynamic, reaching 13.7%. According to data from the EC, Germany had the smallest growth (+2.8%), followed by Slovakia (+3.0%). The weakness of the German recovery is primarily due to problems in the automotive sector, further constrained by government restrictions and consumer caution. A series of tensions in the supply chain for parts and components also played a part. The strongest-growing economies in 2021 were those of Croatia (+10.5%), Greece (+8.5%), Luxembourg (+7.0%) and Slovenia (+6.9%).

Economic situation in Poland in 2021

In 2021, the Polish economy was emerging from the pandemic bottom formed the year before (GDP in 2020 in real terms contracted by 2.5%). The restrictions on social and economic life (which were greatest in the first months of the year) were mostly less restrictive than in the corresponding period of 2020, when an epidemic state was introduced in the country. The situation in the labour market also improved, however, a gradual increase in inflation was observed throughout the year.

According to preliminary estimates from the Central Statistical Office, Poland's GDP grew by 5.7% in real terms in 2021. Thus, it was one of the highest growth rates since 2007, when it had exceeded 7%. In 2021, domestic demand was the main driver of economic growth. Both consumption and investment demand had a positive effect. Domestic demand was 8.2% higher than in 2020. Total consumption grew by 4.8% (a year ago it decreased by 1.1%), of which consumption in the household sector increased by 6.2%. Gross expenditures on tangible assets went up by 8.0%.

The upwardly revised figures presented by the European Commission show a 4.9% GDP rebound in Poland in 2021. The EC saw a rebound in the first half of the year and expects growth to remain robust in the years ahead, despite supply-side disruptions and soaring commodity prices, driven mainly by declining household savings and rapid investment growth. Estimates for 2022-2023 show the Polish economy growing by 5.2% and 4.4%, respectively.

Last year, not only the domestic economy but also the economies of other countries were supported by huge fiscal packages and adapted to administrative constraints. Economists' claims that Poland's GDP would recover in 2021 from the losses caused by the pandemic and that thanks to the "unfreezing" of the economy, an important component of GDP, namely investment, will gain in importance, were thus confirmed.

The Polish economy's strong dependence on and close links to the European Union - which in turn depends on global markets - will remain the key factors driving the direction and pace of growth of the national economy. For Jastrzębska Spółka Węglowa, of key significance are those areas of the economic environment that can substantially impact the shape of the Group's further development, i.e. the coking coal, coke and steel markets.

Steel,coal and coke market

Steel market

Following the pandemic, most of the previously switched-off furnaces in Europe systematically returned to operation in the third and fourth quarters of 2020. This was significant for the industry's performance throughout 2021.

High steel prices and margins in the steel industry, together with rising demand, encouraged an increase in supply through capacity utilisation. Thus, in 2021, the margins of steelmakers based on blast furnace technology were at very high levels - not seen since the boom before the global crisis in 2008. The steel industry's EBITDA over the past 15 years has averaged 6.5%, and reached close to 40% in 2021 in Europe and US.

Blast-furnace (BOF) technology is the dominant steelmaking process in Europe and in the world, accounting for more than 73% of the global steel output. Electric furnace (EAF) production accounts for approx. 26% of crude steel production.

World crude steel production in 2021 reached 1.95 billion tonnes, a 3.7% increase from the preceding year. Only a few countries recorded year-on-year declines in production, however, among them was China, where a total of 1.03 billion tonnes of crude steel was produced, 3.0% less than a year ago. China's crude steel production accounted for 53% of the total steel produced globally, compared to 56.6% in 2020 (in 2019, the share of Chinese production was also close to 53%). India produced 118.1 mt of steel last year, up by 17.8% y/y. Japan produced 96.3 mt of steel, a 15.8% increase from 2020. Other major producers also recorded production growth: US 86 mt (+18.3%), Russia 76 mt (+6.1%), South Korea 70.6 mt (+5.2%), Turkey 40.4 mt (+12.7%), Germany 40.1 mt (+12.3%).

Steel production in European steel mills (EU27) in 2021 stood at 152.5 mt, registering an increase of 15.4% compared to the previous year. The region's largest producer, Germany, produced 40.1 mt of steel, which is 12.3% more than in 2020. Italy, the second largest steelmaker in the region, produced 24.4 mt, a 19.7% increase y/y. This was followed by Spain, which produced 14 mt, up 27.7%, and France with 13.9 mt, up 20.3% year-on-year. Crude steel production in Poland in 2021 grew by "only" 6.5% to 8.4 mt.

Eurofer estimates that apparent steel consumption in the EU increased by 13% in 2021. The market faced disruptions in global supply chains that severely affected demand in steel-consuming sectors. An example is the persistent semiconductor shortage in 2021, not only in Europe but also worldwide, which hampered production growth in the automotive sector.

Steel production and prices of steel products in EU

Chart. Steel production [million tons]

Chart. Steel prices on the European market [USD / t]

Coking coal market

The metallurgical (coking) coal market is global, the prices of seaborne metallurgical (coking) coal are shaped mainly by relations between Australian suppliers and Asian customers. However, since November 2020 China's import policy towards Australian coal has altered these flows. Two separate trade markets were thus created: the traditional FOB Australia market for regions outside China - potentially served by all overseas producers but the only market for Australian products; and the CFR China market - served only by producers outside Australia (mainly US and Canada).

Australian coking coal shipments to China have averaged 40 mt a year over the past five years, accounting for just over a fifth of all Australian exports. The lack of exports to China was offset by higher exports to India, Japan, South Korea and Vietnam as well as European countries.

Rising steel production - in the process of economic recovery after slowdowns caused by pandemic restrictions - generated strong demand for coking coal in 2021. At the same time, the supply of this raw material was limited by production difficulties, transport problems as well as weather difficulties and disasters at the main suppliers to the overseas market.

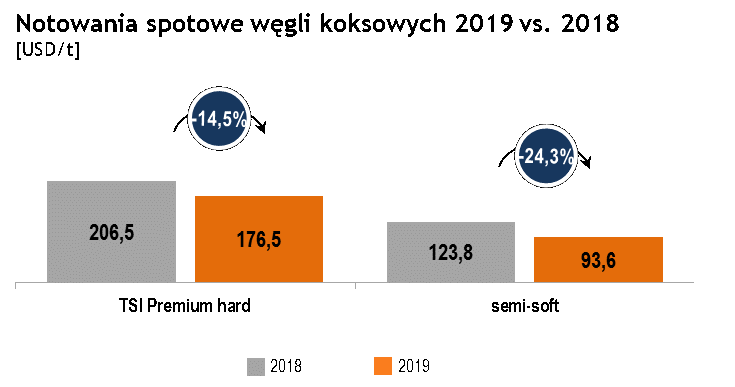

Coal prices remained low until April 2021. The average TSI Premium Hard Coking Coal index price for Q1 2021 was 127.57 USD/t FOB Australia. From the end of April 2021, a clear increase in demand with simultaneous supply constraints began, resulting in successive increases in coking coal prices, which boosted its quotations in subsequent quarters of 2021 to 137.46 USD/t, 263.66 USD/t and 368.67 USD/t FOB Australia, respectively.

Demand for coking coal was high not only from China but also from European and South American countries. The recovery in demand for coking coal in countries excluding China narrowed the spread between quotations in the Asian and Atlantic coking coal markets. Coking coal prices were also bolstered by continuing supply constraints in China, Australia, Canada, Russia, Colombia and Mongolia, the main producers and suppliers of this raw material. In light of the poor availability of supply in the overseas market, subsequent spot market transactions were made at higher prices, which in turn shaped the levels of global indices. The overseas coking coal market entered Q4 2021 with record high price levels on both a CFR China and FOB Australia and FOB US basis. Quotations on a CFR China basis exceeded 600 USD/t and on a FOB Australia basis 408 USD/t at the time. At the end of December 2021, the TSI Premium Hard Coking Coal index value was 357.25 USD/t FOB Australia, bringing the full-year average to 225.8 USD/t.

Chart. JSW's metallurgical coal (coke) price in relation to quotations

* considering the prices affecting JSW’s prices in a given year (the average price in October of last year - November of the current year), the growth in the average reference price for coking coal in 2021 versus 2020 was +48% (TSI Premium Hard: USD 129 in 2020; USD 191 in 2021)

JSW Group's coal prices are shaped based on published price indexes, taking into account the quality differences of the Group's coal compared to index coals (from Australia) and a geographical premium. The relationship between the average price of coking coal sold by the Group to external buyers converted to USD at the average National Bank of Poland rate from a given quarter and the average TSI Premium Hard prices for 5 months (covering the previous quarter and the first two months of the current quarter) is presented in the chart below.

Chart. Relationships between JSW's metallurgical coal (coke) prices and quotations

* average price for TSI Premium HCC for 5 months includes the previous quarter and two first months of the current quarter

Thermal coal market

Jastrzębska Spółka Węglowa is not a major producer of thermal coal in Poland and is perceived by customers in the domestic utility power segment as a supplementary supplier (JSW S.A.'s share in thermal coal production in Poland is approximately 6%), which is why it is forced to adapt to market realities without being able to create them on its own. The utility power generation sector requires prices to be set for periods of at least six months/year. This is why coal prices for the domestic power industry follow to a limited extent the global trends of price indexes for spot transactions. ARA prices affect the Polish market, but in the longer term, after about a year. The price of thermal coal in Poland is largely driven by the situation on the domestic market and competition between domestic producers. The thermal coal market in Poland is largely dependent on the domestic economic situation, weather conditions, energy policy (prices of electricity, use of biomass, lignite-based electricity generation, share of subsidised renewable energy).

According to data from Polskie Sieci Elektroenergetyczne, domestic electricity output in 2021 increased by 14%, reaching 173.6 TWh. The main growth factor was the economic recovery and unfreezing after the crisis caused by the SARS-CoV-2 virus pandemic. Utility power plants accounted for the largest share of electricity generation in 2021 with 89.1% (vs. 82.3% a year earlier), dominated by hard coal 53.6% (+6.6 percentage points) and lignite 26.1% (+1.2pp). There was a slight decrease to 7.7% (-1.2pp) for natural gas. In terms of green energy, wind power plants and other renewables contributed almost 11% to energy production (+0.2pp).

In 2021, the PSCMI1 index, reflecting the price of thermal coal in sales to the domestic utility and industrial power sector, fell by 6.4% to 248.57 PLN/t (11.42 PLN/GJ) compared to 2020, and was also 4.9% lower than two years earlier. The following chart presents the relation between the quarterly prices for thermal coal sold by the Group and the PSCMI1 index.

Chart. JSW steam coal prices in relation to the PSCMI quotation 1 [PLN/t]

Source: ARP,www.polskirynekwegla.pl, dane JSW

In contrast to domestic price declines, the average annual price for pulverised coal imported by sea to Western and Northern European countries via ARA ports (Amsterdam, Rotterdam, Antwerp) increased by 146.6% in 2021 to 123.3 USD/t (2020: 50.0 USD/t).

Coke market

Just as in the case of coking coal, the coke market is global. Demand for coke largely depends on the level of steel production in the basic oxygen furnace process (BOF), which currently accounts for approx. 73% of global steel production. Nearly 26% of global steel output comes from electric arc furnaces (EAF). Other processes, such as direct reduced iron, account for a margin part of steel output. In China, nearly 90% of steel is produced in blast furnaces, while in the EU this is approx. 58%, below the global average.

Global coke production in 2021 went up 4% year-on-year to 718 mt. China produced approx. 478 mt, which represents around 67% of global coke production, with China recording a 2% increase over last year's output. The recovery of steel production led to a return in demand for coke in European countries, traditionally being the largest importers. In 2021, coke consumption in Europe grew by 10% compared to the previous year and amounted to approx. 46 mt, while the production of coke in that period also increased by 10% to approx. 44 mt. Poland is a major external supplier of coke in the EU. Because the coke market is global, coke from Poland competes with coke supplies not just from Europe but from all over the world, including China, Russia and Colombia. Prices for blast-furnace coke on the European market averaged 460 USD/t in 2021, denoting a 92.6% increase in comparison to 238.8 USD/t in 2020.

Chart. Coke price quotations **

** taking into account the quotations affecting JSW’s prices in a given year (the average price from Q4 2020 - Q3 2021), the increase in the average reference price of coke in 2021 versus 2020 was +48% (blast furnace coke on the European Market: USD 244 in 2020; USD 362 in 2021).

In addition, in 2021, the relation between blast furnace coke prices on the European market and contract prices for premium hard coking coal remained at a very favourable level ensuring high profitability of coking plant operations.

Chart. JSW’s coking coal prices in relation to TSI premium HCC prices [USD/t]

* average price for TSI Premium HCC for 5 months includes the previous quarter and two first months of the current quarter

Chart. JSW’s coke prices in relation to prices blast furnace coke prices on the European market [USD/t]

* coke prices are set at the turn of each quarter in order to reflect the market terms of the negotiations. The optimal approach is to compare the prices obtained in the respective quarter with the average quotations from the previous quarter

Source: Platts, Coke & Anthracite Market Report, JSW's data